Update (Feb 26) – It turns out that we failed to be clear on something pretty important here… rendering our headline ironically pretty apt. Maybe you really can’tbelieve Belize’s disavowal of ratable payment on its bonds.

OK, so here’s the section on pari passu language in the new bonds’ Offering Memorandum:

“To ensure clarity on the point, Belize does not understand…” and so on.

Well, a couple of observers have pointed out to us that bondholders might not necessarily agree with Belize’s understanding. In other words, the disavowal might not protect Belize from legal challenge in the future, if it defaults on the new bonds. Why? Because Belize put the ratable payments disavowal in its offering memorandum — not in the actual contract for the new bonds. We should have made that clearer originally.

“Is that disavowal… important for the restructured creditors [to have]?,” we asked below. Well, no. They didn’t agree to put it into the contract, which is a sign that the bondholders didn’t agree with Belize’s interpretation in the first place, and did not wish to discard ratable payment.

That’s important to clear up, but it’s also interesting given what is really the most critical debate on obliging sovereigns to pay their bonds ratably.

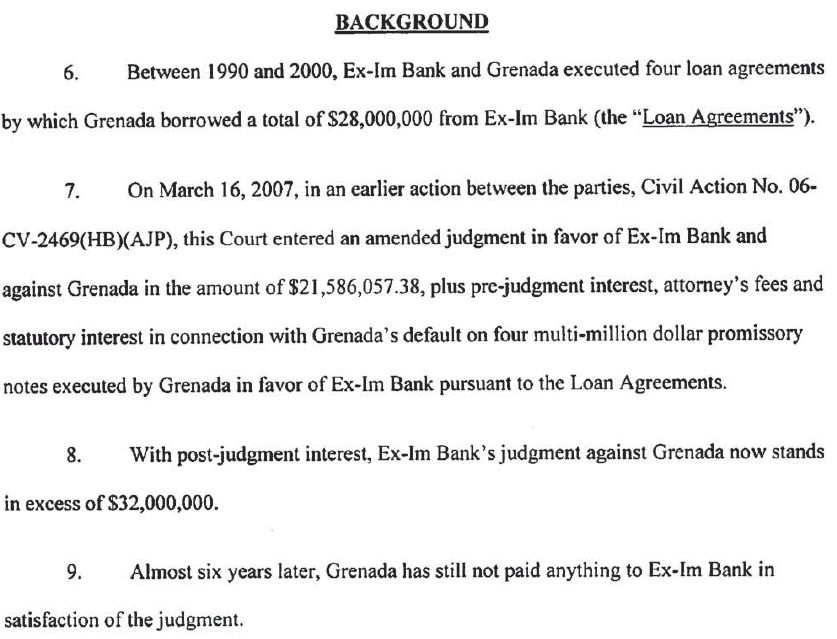

The argument is about whether such an obligation can be inferred from a provision for equal treatment without the words ‘ratable payment’ having to be spelled out — or whether it needs sovereigns to issue debt with specific language attached. Beyond Belize, a case to consider might be Italy’s

sale in 2010 of New York law debt with a promise to “pay amounts due… equally and ratably”.

At the same time, it’s worth noting that the Belize contract could arguably be called a ‘narrow’ pari passu clause because it talks about ‘ranking’ rather than ‘payment’ in terms of equal treatment. The offering memo itself has also come from a hotly-negotiated restructuring, emerging after extensive discussion on terms. But there’s a difference between a contract between two sides, and Belize’s interpretation of the contract given in an offering memo drawn up by its lawyers, or in a resolution of its own legislature.

We can also bring it back to events tomorrow in the Thurgood Marshall US courthouse, and whether Argentina has

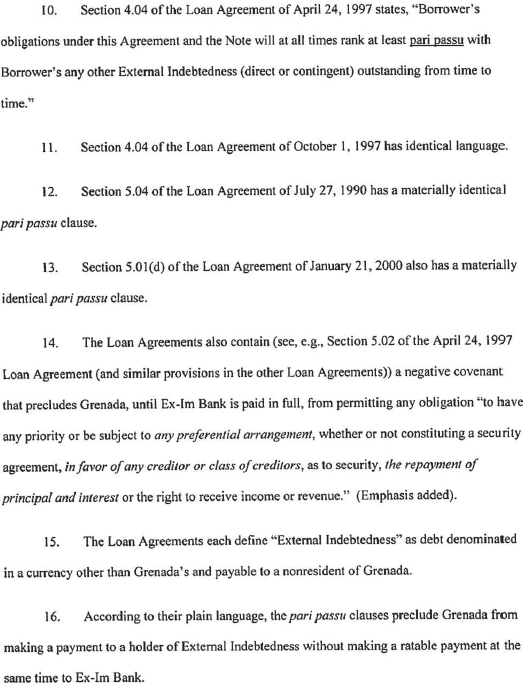

much chance convincing the Second Circuit. In October, the court

agreed with a remedy of ratable payment for Argentina’s bond holdouts because it saw the dispute as a “simple question of contract interpretation.” Note the focus on contract.

Original post below the line.

_____________________________________________

It’s the week of the big hearing in the pari passu saga.

Argentina (plus the bondholders who agreed to be restructured between 2005 and 2010, plus Bank of New York) will try to convince the Second Circuit that it should change

an order for the country to pay holdouts

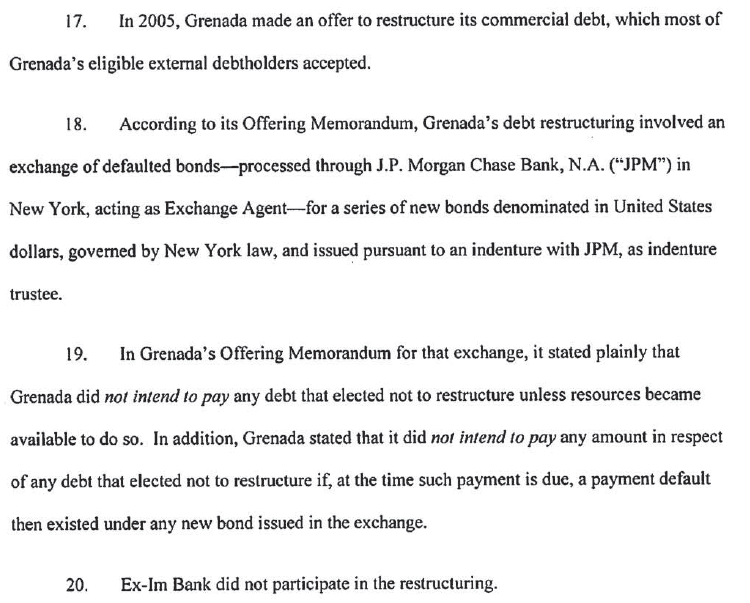

ratably as a remedy for breaching their bond contract

. ‘Ratable’ is a term with a

controversial history in sovereign debt but it basically means paying each creditor on the same basis, not paying one after the other.

Well, speaking of ratable payment… we’d just like to point something out from the Belize debt restructuring, which has been

going on while the pari passu saga has trundled through courts:

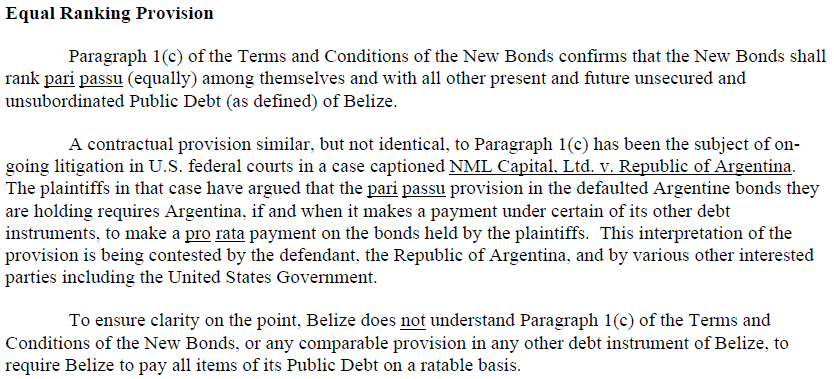

Status of the New Bonds

The New Bonds will be general, direct, unconditional, unsubordinated and unsecured obligations of Belize and will rank at least equally among themselves and with all of Belize’s existing and future unsecured and unsubordinated indebtedness (it being understood that this equal ranking status shall not require Belize to pay all items of its bond indebtedness on a ratable basis).

A mere sub-clause, but what a sub-clause.

That wording comes from the Belize National Assembly’s

resolution, passed this month, which authorises the government to issue new debt to bondholders. It includes the bonds’ basic terms and conditions (unfortunately the full Offering Memorandum itself is hard to track down — the offer period is still open), but it’s really that direct disavowal of ratable payment which is special.

Particularly in this restructuring.

Belize could have ended up as a pretty acrimonious default. It started out as one: the government played hardball last year, through missing a coupon payment on its $550m ‘Superbond’ — the result of its last debt restructuring, back in 2007 — and generally just not being nice to its creditors. The mood got better after the creditors formed a committee, allowing everyone to sit down to argue about economic projections and the chances of debt repayment.

Still, while Belize’s offer will be getting the acceptance

it needs, the bond terms appear to contain some fairly innovative protections to make sure Belize can’t play hardball again. Joe Kogan of Scotiabank has observed that creditors get to claw back the 10 per cent reduction in bond principal which they’ve agreed to, if Belize fails to make a payment within the next decade. There also seems to be an account set aside for paying the expenses of a future creditor committee. As Kogan also notes, these protections could ultimately depend on being able to attach Belizean assets to force these payments —

c’est la vie when litigating against a sovereign — but they’re nice to have.

So in this context Belize says that it doesn’t consider itself to have an obligation to pay ratably under these bonds. Is that disavowal important for Belize to have? Or important for the

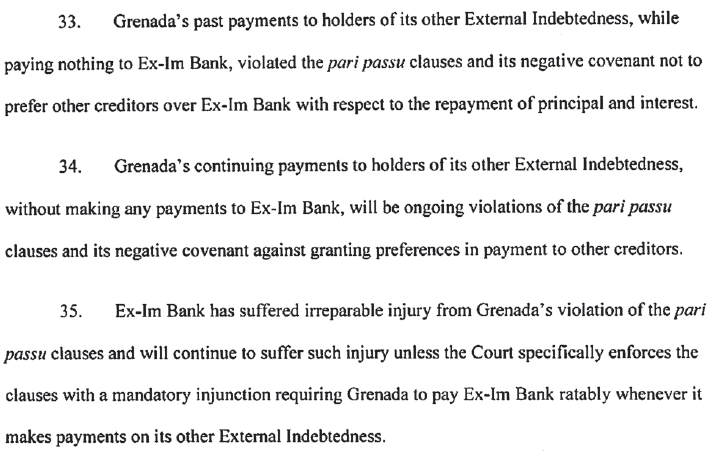

restructured creditors? Will it in some way shape the legacy of the pari passu saga?

Sovereign debt restructurings don’t come around very often, even these days. The new Belize bonds come five months after the Second Circuit first confirmed ratable payment for Argentina’s holdouts, making them (we think) the first debt exchange to react to the court’s decision. Some sovereigns have since sold New York law bonds

warning that the Argentine litigation has now created legal risk within pari passu clauses, but unlike Belize they didn’t go into the weeds of ratable payment.

Maybe its disavowal means the Second Circuit really should revisit the Argentine order after all.

But then Argentina has previously argued to courts that no sovereign debtor in its right mind would ever agree to ratable payment, given the power it would give to holdouts. Is that right? The Belizean rewrite suggests that sovereigns do recognise the ratable implications of a promise to pay pari passu, and that they can easily adapt bond contracts to shut those implications down. Even in a sovereign restructuring. Or, rather, especially in a sovereign restructuring.