| Grenada 25 SU Reg S (DUS) - 15.09.2025 Price: 48 USD Chg. (in%): Bonds:Government of Grenada:2005-15.9.25 Reg S Step Up (UNSUBORDINATED)

|

Klage Im-Ex-Bank-China v Grenada

http://ftalphaville.ft.com/files/2013/03/13cv014501.pdf

Some excerpts from a lawsuit filed by the Export-Import Bank of China (Taipei) against Grenada in a United States district court on March 4, 2013…

If you have been following the pari passu saga on ratable payment of sovereign debt — they tell their own story. (Click to enlarge all images.)

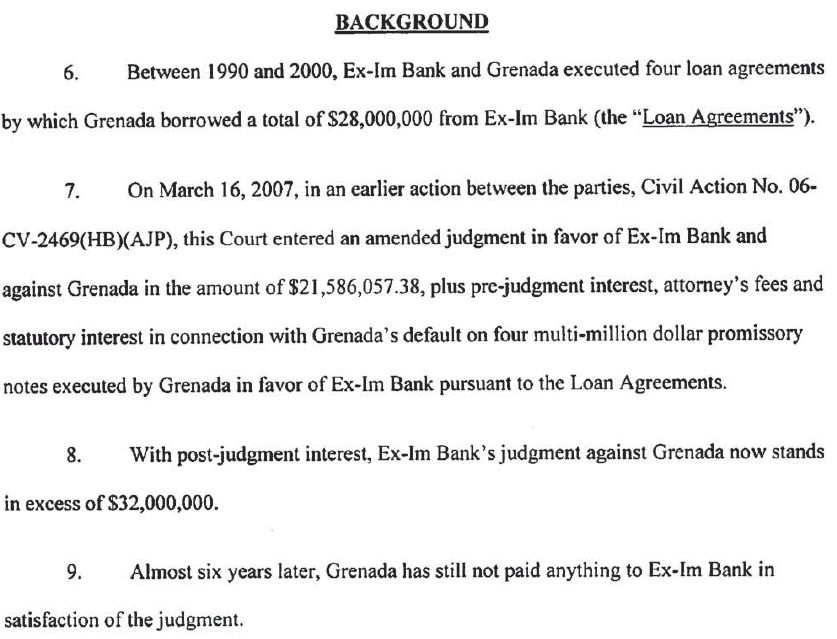

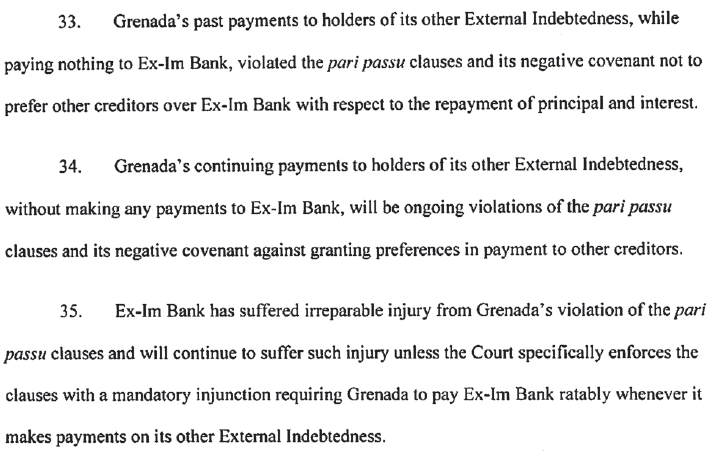

1.) Ex-Im Bank already has a judgement on $32m of debt defaulted on by Grenada.

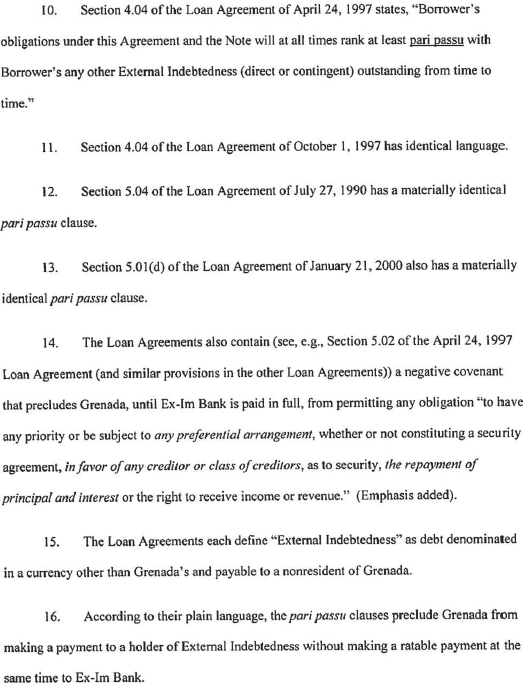

2.) The loan debt had a pari passu clause, and negative pledge language.

3.) Let’s just spell that last bit out, as cited by Ex-Im Bank.

According to their plain language, the pari passu clauses preclude Grenada from making a ratable payment to a holder of External Indebtedness without making a ratable payment at the same time to Ex-Im Bank.

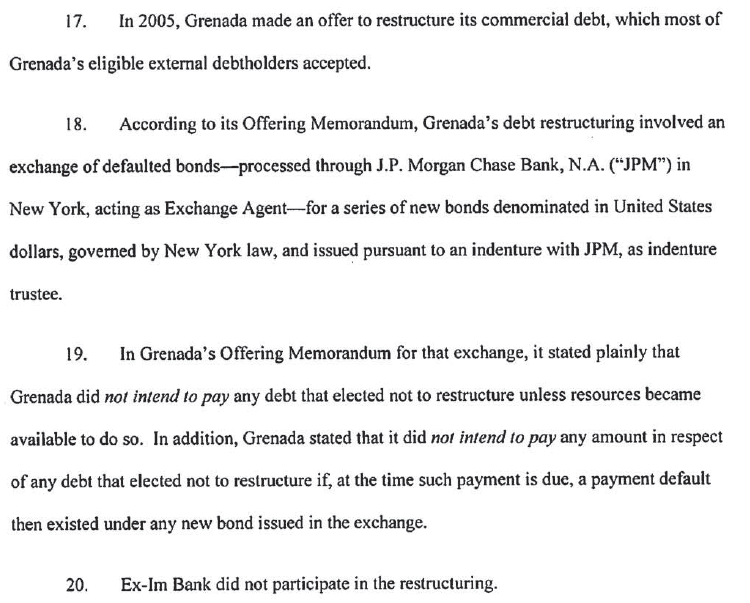

4.) Ex-Im Bank stayed out of Grenada’s 2005 debt restructuring.

5.) It has been watching Grenada pay the people who did restructure.

6.) Bank of New York handled some of that dough. Bank of New York lives in New York.

7.) Ex-Im Bank is now coming after these payments to Grenada’s restructured bondholders. (Hello, intercreditor consequences of ratable payment.)

8.) And Ex-Im Bank’s citing equity.

They didn’t even wait for a final Second Circuit ruling on Argentina making ratable payments to its holdouts. (Why should they, actually? The implications of ratable payment are arguably clear.)

Incidentally observe point 1) there, that Ex-Im Bank is exploring this avenue having already won judgement against Grenada. (The story of their dispute is a long one.)

The $1.3bn of claims involved in NML’s pari passu litigation against Argentina were not judgement debts. Nevertheless. EM Ltd, which holds a prior judgement against Argentina, said (in a pro-holdout amicus brief) that while “the District Court has not yet been asked to address whether the Equal Treatment Provision can be used to enforce an existing judgment,” EM Ltd “believes that the Equal Treatment Provision applies with identical force in the post-judgment context”.

And now we have crossed into new territory.

Post your own comment

Sorted by oldest first | Sort by newest first

- Reportplasmaj | March 6 6:46pm | PermalinkExcept when they got their judgment they gave up their rights with respect to the bonds, including pari passu. Citi had a good piece explaining that.

- ReportJorge Marquez | March 6 7:31pm | PermalinkCan you link that plasmaj? Or, at least, elaborate on what you just said. I'm intrigued...

- Reportanoldbanker | March 7 2:36pm | PermalinkArgentina's equal treatment clause applies to payments; Grenada's only applies to ranking of the different debts. This is a critical distinction thoroughly discussed in academic analyses of pari passu.

- ReportJoseph Cotterill, FT | March 7 5:20pm | Permalinkanoldbanker & plasmaj - Yep. Sure, it's not a particularly cast-iron case in itself (I think) because of the judgement issue and the lack of payments language. But it is striking and a sign of an important change that they thought they can even try.

Keine Kommentare:

Kommentar veröffentlichen